Market Concentration: Only a Few Large Players Are Winning in E-Commerce

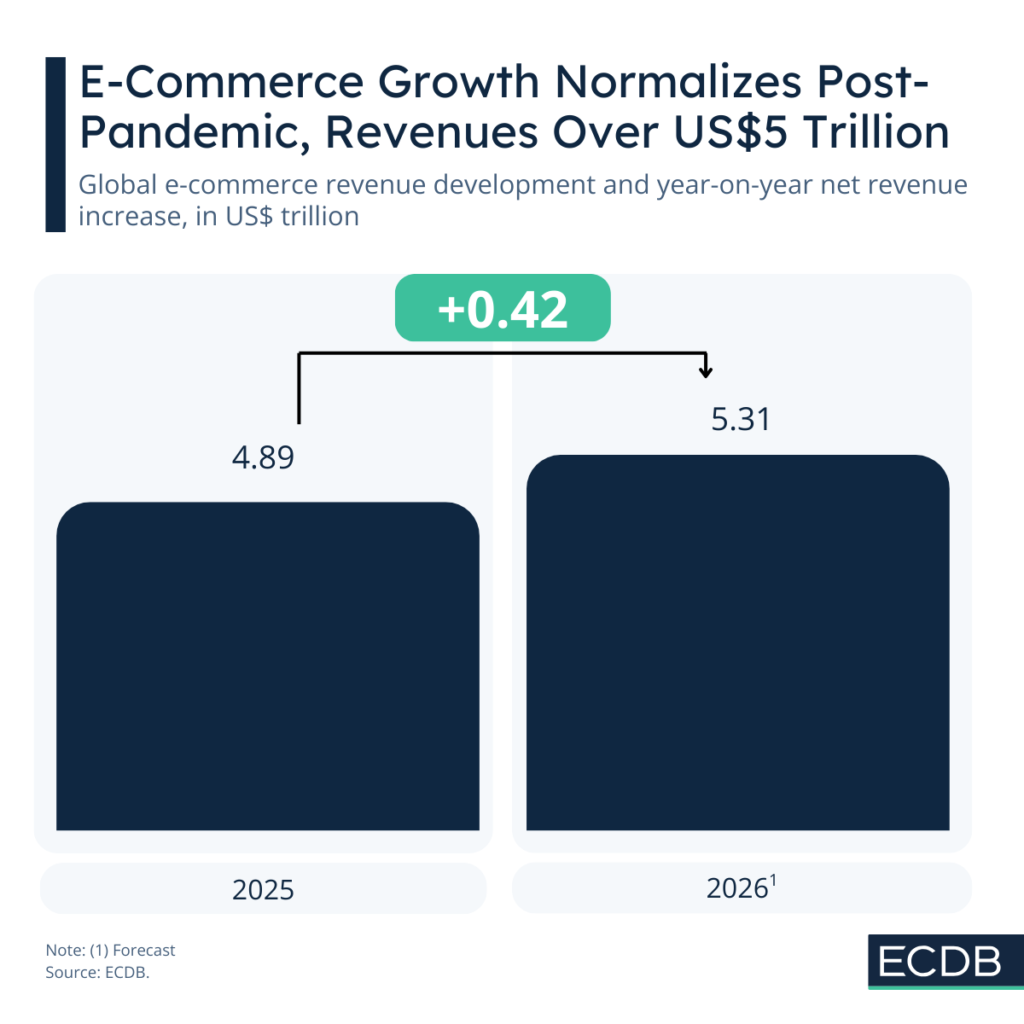

The years of stagnation in e-commerce are over. According to ECDB, growth is expected to regain its former momentum in 2026. A new global threshold of US$5 trillion in revenues is expected to be surpassed this year. That marks a net increase of US$421 billion compared to 2025.

But this growth is far from evenly distributed. A closer look at where global e-commerce growth originates reveals a familiar pattern: the same two or three markets consistently account for the lion’s share of revenue gains.

This points to a clear trend toward market concentration, one of many insights found in the report ECDB Global E-Commerce Compass. In the following joint analysis by ECDB and Digital Commerce Finland, we examine who the concentration centers around the most.

Global E-Commerce Surpasses US$5 Trillion Amid Market Recovery

A normalization of e-commerce revenues after the pandemic peaks led to temporary dips in the following years. That phase now appears to be over. Growth has rebounded, and the industry is reaching new milestones.

In 2026, global e-commerce revenues are forecast to exceed US$5 trillion. More precisely, analysts expect global e-commerce to generate US$5.31 trillion this year. This places the sector on par with the GDP of major economies like Germany or Japan.

In absolute terms, growth since 2025 denotes a net increase of US$421 billion. But its distribution tells a more nuanced story.

World E-Commerce Growth Is Concentrated in a Few Markets

Net growth highlights where revenue is actually being added in absolute terms. This stands in contrast to relative growth, which tends to spotlight smaller markets due to higher percentage increases, even if their overall contribution remains limited.

Take the net growth of this year as an illustration of this dynamic. Of the US$421 billion increase in revenues, 42% come from the largest e-commerce market Greater China. The United States follow by accounting for 19% of net revenue growth. The third-largest market, the United Kingdom, contributed US$12 billion, or 3% to this growth.

Together, the three largest e-commerce markets drive 64% of global e-commerce growth. The remaining US$153 billion is distributed across the rest of the world.

A percentage-only based depiction therefore leaves out the scale and concentration effects that determine where most of the absolute revenue gains are generated. This affects e-commerce retailers as well.

Chinese E-Commerce Giants and Their International Rise

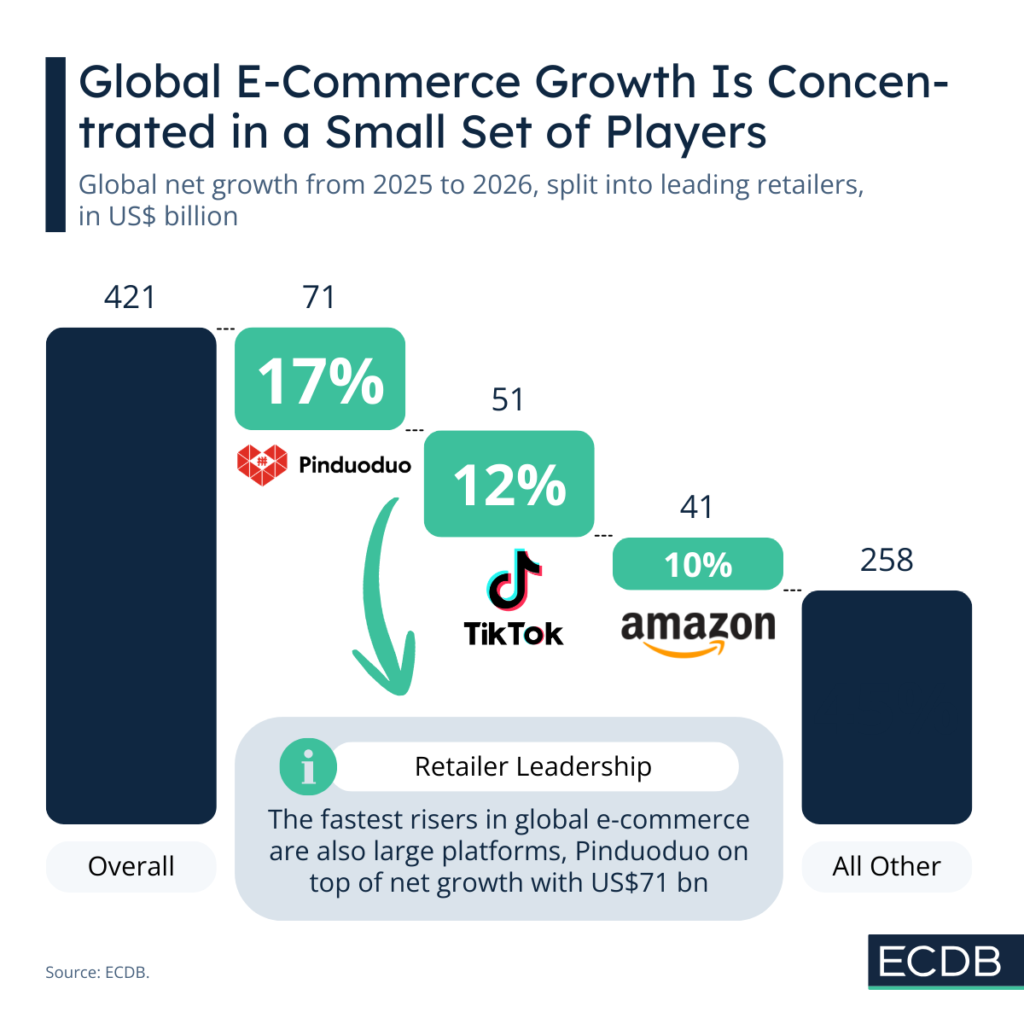

At the company level, concentration is somewhat less pronounced, but still significant. The three largest players account for 39% of global net revenue growth. This distribution between Pinduoduo, TikTok (Douyin) and Amazon leaves more room for other players to contribute.

China’s outstanding role is supported nonetheless in this depiction. The two leading retailers, Pinduoduo and Douyin, are both top Chinese players with significant ventures abroad. Pinduoduo’s sister platform, Temu, is rapidly gaining ground across multiple e-commerce markets; in Finland, for example, it currently ranks as the leading platform.

Similarly, Douyin is expanding internationally through TikTok Shop, with a strong presence in Southeast Asia and the United States. Its footprint in Europe is growing as well, though it has yet to achieve the same level of traction.

Amazon, by contrast, remains the global frontrunner. Its presence in China and Asia more broadly is relatively limited. It continues to be a major driver of US e-commerce concentration, even as the United States lags behind China overall.

Growth Patterns Reinforce the Dominance of China and the United States

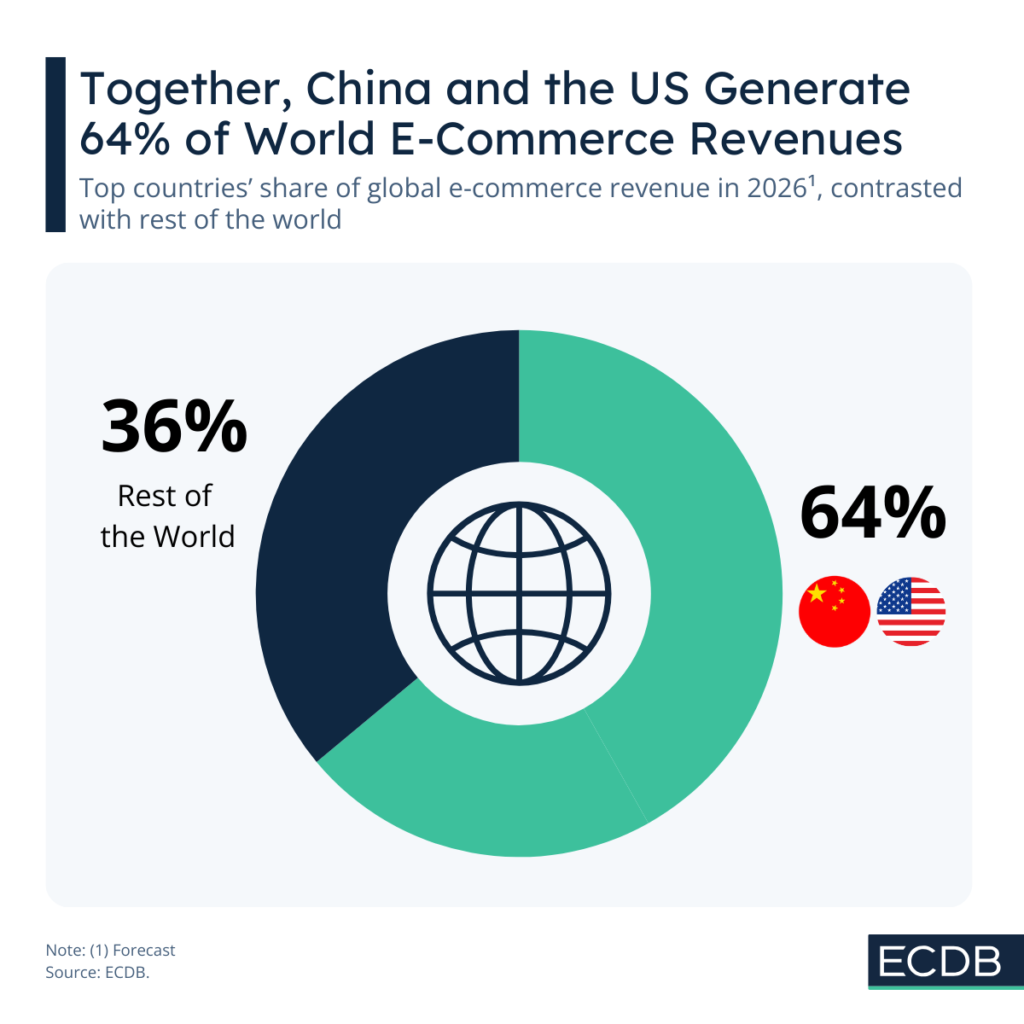

While growth dynamics highlight change, total market size reflects continuity. Global e-commerce remains dominated by two players: China and the United States.

China is in a league of its own, with market revenues of US$2.2 trillion and year-on-year growth of 8.6%. The United States also significantly outpace other competitors, but still lag far behind China by approximately US$1 trillion.

China is ahead of the United States in terms of growth as well, at 8.6% year-on-year increases, compared to 7.4%. Among the top 10 countries, India and Russia mark the fastest growing ones, at respective rates of 13.2% and 11.6%.

Despite this, none of the lower-ranked markets come close to the scale of the two leading economies. Even high-growth emerging players such as India, Russia, and Brazil, despite their large consumer bases, remain far behind in absolute terms.

In effect, concentration reinforces itself: leading markets capture the largest share of net revenue growth, further cementing their dominant positions.

China and the US Account for 64% of Global E-Commerce Revenues

Relatively, that concentration holds up: 64% of e-commerce revenues in the world are generated by China and the United States. The remaining 36% belong to the rest of the world.

This fact has an important implication on current political developments, because tariffs and trade barriers reinforce the present concentration further by making cross-border competition more costly for smaller or emerging markets.

Outlook: Market Concentration Defines World E-Commerce

Market concentration is a defining force in e-commerce. The dominance of China and the United States is reflected twofold: On the one hand through current market size and on the other through new revenue contributions. As these two markets capture the majority of incremental growth, their lead over the rest of the world widens further.

For companies, success in global e-commerce will depend on how effectively they position themselves within or alongside dominant ecosystems. For smaller and emerging markets, the challenge lies in remaining competitive despite structural disadvantages that are amplified by scale and, increasingly, by geopolitical factors.If you are interested in more analyses like these, visit Friedrich Schwandt’s talk at the eCom Summit on May 21st!